Organizations that produce unique or custom products or services typically use a job-order costing system. For example, a construction company specializing in new home construction uses a job-order costing system. The costs for direct material, direct labor, and manufacturing overhead is assigned directly to the homes using the materials or labor.

Direct materials

Non-manufacturing costs include selling and administrative expenses that are not directly related to producing a specific product or service. Failure to include these costs in the cost of production can lead to inaccurate pricing decisions and profitability analyses. Direct expenses are costs directly related to a product’s production but are not considered material or labor costs. Examples of direct expenses include special tooling required for a specific job or the cost of subcontracting work to another company.

Direct Expenses

Job order costing is often presented as a tool for product-based businesses. Costs typically break down differently, though, with labor being very important and materials not as much. Using job order costing over time will develop a historical record of all projects you’ve completed. This information can be revisited monthly, quarterly, and yearly to evaluate the company’s efficiency and identify areas to reduce costs. Job order costing requires a certain amount of detail, including the tracking of labor and machine hours. This way, you can determine which pieces of equipment or which employees fall below the company standard.

Video Illustration 2-5: Computing multiple predetermined manufacturing overhead rates LO6

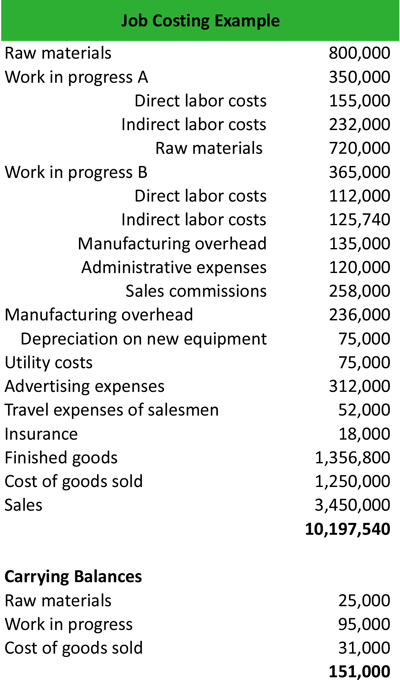

The incurred indirect costs should be allocated to the job based on previous examples. In other words, the cost for this job is assigned based on the costs incurred in the past while doing a similar job. They’re provided as an estimate, and should be adjusted in the final stages of production based on any additional indirect costs which add up during the production process. These costs include the cost of manufacturing equipment, the electricity used to run the equipment, utility bills, and depreciation of machines. Actual costing is a simplistic and accurate way of keeping track of job costs.

DS will charge an amount equal to the cost of the airplane plus a 30% profit margin on cost to the government of Pakistan. This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions. Process costing, on the other hand, is used in situations where all the products being manufactured are similar. If any surplus material is returned from the job to the stores, the job account is given due credit for the value of the same. If any special material is purchased for a job, it is directly charged to the job on the basis of an invoice.

- An accountant can help you analyze your business and develop a specific approach to overhead.

- Direct materials are raw materials costs that can be easily and economically traced to the production of the product.

- For example, a doctor’s office may order patients based on the purpose of visits and the cost of treatments administered.

- The responsibility of preparing the BOM lies with the production planning department.

- Under this system, costs are assigned to jobs based on the number of direct labor hours required to manufacture each job.

Job sheets allow you to keep an eye on how your machinery functions and also monitor the productivity of your employees. Keeping you one step ahead of the maintenance cycles for your expensive machinery and allowing you to take necessary steps to boost employee productivity.

This video on how drumsticks are made shows the production process for drumsticks at one company, starting with the raw wood and ending with packaging. You’ll also learn the concepts of conversion costs and equivalent units of production and how to use these for calculating the unit and total cost of items produced using a process costing system. Using job order costing to determine the profitability how to calculate vacation accruals free pto calculator of each project gives you valuable insight into the value of each client and can help you package and price your services. Calculating estimated activity is done by adding the activities that apply to overhead costs, such as labor hours. The hours per activity are then multiplied by the overhead rate per activity, arriving at the overhead cost per activity for the job order.

An organization with multiple departments or processes may choose to apply manufacturing overhead using multiple predetermined manufacturing overhead rates. Process costing is used most often when manufacturing a product in batches. Each department or production process or batch process tracks its direct material and direct labor costs as well as the number of units in production. The actual cost to produce each unit through a process costing system varies, but the average result is an adequate determination of the cost for each manufactured unit.

An accountant can help you analyze your business and develop a specific approach to overhead. Both process costing and job order costing maintain the costs of direct material, direct labor, and manufacturing overhead. Job order costing tracks prime costs to assign direct material and direct labor to individual products (jobs). Process costing also tracks prime costs to assign direct material and direct labor to each production department (batch). Manufacturing overhead is another cost of production, and it is applied to products (job order) or departments (process) based on an appropriate activity base. The key to job order costing success is precise documentation on your direct materials, overhead costs, and direct labor hours that contributed to completing a project.

In the preceding sections, an organization-wide predetermined manufacturing overhead rate was calculated. Many organizations have multiple departments or processes that consume different amounts of manufacturing overhead resources at different rates. In these organizations, a single manufacturing overhead rate, while more simplistic, may not accurately apply overhead to the final product.

Recent Comments